Suprajit Industries - An old note

Disclaimer: I am not invested in Suprajit. I am not an investment advisor. This is an old post I wrote in 2019.

I wrote this note on Suprajit in 2019 during my stint with Intelligent Fanatics LLC. I have not followed Suprajit since then as I never found the business to be cheap. However, I do believe there is a lot to learn from the way the management runs the business. While the numbers are not updated, I think the essence of the business remains the same.

One investing approach is finding promising candidates in sectors / industries that are going through distress. One sector (of the many) that is going through stress currently (in 2019) is the automobile industry in India. So I thought it would be interesting to trawl the listed companies in the automobile sector to find out interesting candidates.

In my search, I keep an eye out for something that is really out of the ordinary. One way to expose yourself to serendipity is to randomly read annual reports of companies. I start with the latest annual report. Here are a couple of charts that piqued our interest in the annual report of Suprajit Engineering, an auto component company based out of India with a market cap of ~2300cr ($300 million).

First, it is uncommon for companies in India to show their evolution from 2002.

Second, there seems to be steady compensation for fragility. What was predominantly a 2-wheeler focused business supplying only to OEMs (Original Equipment Manufacturers) has evolved into a business that generates almost equal revenues from multiple segments. Also, what was primarily a domestic business today generates around 40% of revenues globally.

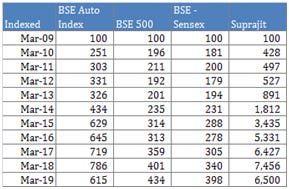

Third is the table below. Once again, you hardly see any company compare themselves thus.

Basically, Rs. 100 would have become - a cool Rs 615 by 2019 if invested in the auto index in 2009, Rs 434 if invested in the BSE 500, Rs 398 if invested in the Sensex and a staggering Rs. 6,500 if invested in Suprajit.

This is, to put it mildly, a stunning out-performance. And Suprajit is in the auto component sector - a sector which doesn’t have a great history due to the extremely weak bargaining power with customers and high competition.

How did Suprajit achieve this then? It was an outcome of steady de-risking, prudent capital allocation and relentless execution of the founder Ajith Kumar Rai and his team at Suprajit.

Beginning:

Suprajit (a combination of Supriya, his wife, and his name) was formed in the 1980s due to Ajith Kumar Rai’s desire to do something on his own. Ajith was from an agricultural family and was very smart academically. He went to Canada to pursue his Masters in Engineering and when he returned he wanted to start his own company. His father-in-law was an eminent professional who was on the Board of a few companies.He put Ajith in touch with Venu Srinivasan of the TVS Group (currently Chairman of TVS Motors). TVS, then and now, is a leading business house from South India focused on the automobile business. They run TVS Motors which is one of the top 2-wheeler and 3-wheeler companies in the country.After the discussion with Mr. Srinivasan, Ajith decided to enter the mechanical cable manufacturing business, as there was only one major domestic manufacturer (Remsons, that began operations in 1965) with the remaining cables imported.

Mechanical cables have certain interesting features. The product is proprietary (designed by the component supplier and not the OEM supplier), safety critical and not interchangeable - unlike for example a bolt or nut. Each cable is designed and manufactured for a particular application. A parking brake cable is different from seat cable. And a parking brake cable of let’s say BMW Mini cannot be used in a BMW One series or any other series, let alone another manufacturer. Also, every product has to go through a long product approval. It can take up to 2 years for each product to successfully reach approval- trial vehicle, prototype, few first batches, road worthy, then pilot. Also, the cost of each cable is at the maximum a few hundred rupees (on average <$10). Thus, it is an essential, safety-critical product at very low price in relation to the total end product.

Ajith Rai did not have the capital to set up a factory at that time and the Karnataka State Financial Corporation came forward with financial assistance. He got a small one acre plot at Bommasandara in the vicinity of Bangalore. He also tied up with TohFon Machine Company Limited (Taiwan) for technical collaboration.

TVS Group: Apart from providing the idea, the TVS Group also agreed to procure cables produced by Suprajit solely based on their assessment of Ajith Rai. TVS also helped Suprajit procure technical know-how from Japanese consultants which helped them in serving TVS in the beginning and then later, other clients as well.The going was quite tough in the beginning as can be expected. Suprajit initially received the orders Remsons, the first company to introduce control cables (a type of cable) in India, couldn’t handle. Originally Remsons was the only company to possess the expertise and the technology to produce a wide variety of cables for the automotive sector. It also had been a TVS supplier for a long time.

Pretty soon, Ajith’s execution skills became evident as Suprajit was able to supply cables with much lower defects at competitive costs promptly. Suprajit became the sole supplier of cables to TVS. Eventually, Suprajit supplied speedometers to TVS vehicles as well.

Around 10 years later TVS again came to Suprajit’s help. Suprajit listed its shares via an initial public offering (IPO) in 1996 as it needed funds to expand its capacity and when the issue was under-subscribed, it was TVS again who came in and subscribed the remaining 10% of the issue.

Relentless execution and Steady derisking:

In his book ‘Zero-to-One’, Peter Thiel provides this advice to businesses:

" Every startup is small at the start. Every monopoly dominates a large share of its market. Therefore, every startup should start with a very small market. Always err on the side of starting too small. The reason is simple: it’s easier to dominate a small market than a large one. If you think your initial market might be too big, it almost certainly is.

The perfect target market for a startup is a small group of particular people concentrated together and served by few or no competitors. Any big market is a bad choice, and a big market already served by competing companies is even worse."

Like Cera, Ajith Rai was focused on ensuring Suprajit focused on just one segment for the first 30 years of its existence - cables. Like Vikram Somany dabbled in certain businesses before putting all his eggs in the Cera basket, Ajith Rai also dabbled for some time in software and chemicals but his predominant energy was on the cables business.

The procurement strategy of the automobile industry is to acquire large volumes from a few suppliers. This allows them to manage the suppliers well in terms of approval, and delivery. Also, with increasing volumes, the auto OEMs demand reduced price per unit. Thus the strategy benefits both OEMs (through reduced costs) and the auto component suppliers themselves (through increased scale).The price per unit of a product in the OEM segment is thus decided by market forces and the supplier does not have much control over it. The only factor in the supplier’s control are internal costs and efficiencies.

Suprajit put tremendous focus on the four attributes that are key for success of any auto component supplier- Quality, Cost, Design, and Delivery. By constant focus on both operational and capital costs, it ensured it remained a low-cost player in the industry. In fact, Suprajit maintains that it has among the lowest cost structures among its competitors. In fact, as Ajith Rai said in a recent conference call, cost reduction was and is a constant endeavor at Suprajit. The reduction in cost is achieved through a number of ways including:

Razor sharp focus on quality, which ensures the best defects per million pieces ratio and reduces wastage.

An extremely efficient manufacturing process that reinforces the large scale of operations that can manufacture a large number of cables in a given period of time, thereby harnessing economies of scale leading to reduced per unit cost.

Low cost automation through in-house efforts to counter increasing employee costs. Suprajit has actually designed and developed low cost automation through in-house efforts. Not many companies would have the imagination or the capability to do this.

It has ensured faster time to maximum efficiency in new plants through the focus on developing simplified, flexible and highly operator friendly processes to achieve zero defect & high productivity.

The relentless, disciplined operational strategy drove strong market share gains for the company. The journey of Suprajit is fascinating for its slow and steady increasing of its circle of competence.

Suprajit’s journey which began with 2 wheelers was instrumental in its success as India is the largest 2 wheeler market in the world. Each 2 wheeler has around 4 to 6 mechanical cables, and the volumes of 2 wheelers has increased tremendously over the last 3 decades. Thus, riding on the tailwind of increased 2 wheeler demand in the country, Suprajit quickly became the largest 2-wheeler cable producer in the country.For the first few years of its existence, it was focused on supplying cables primarily for TVS. But it decided it did not want to be over-reliant on just one customer. Through a short chance meeting with Rajiv Bajaj, Ajith Rai was able to convince the former to give Suprajit a chance. Around this time, it began supplying to Hero Honda as well, which was the major motorcycle player in the country. The advantage of supplying to OEMs, in addition to economies of scale, is that it creates tremendous institutional knowledge of the product.

Subsequently, it entered the automotive space (4 wheeler, CVs). It gained a strong position in this segment by acquiring competitor Shah Concabs in 2002 (see below). For each customer it set up a plant next to the customer’s manufacturing facility so that it could deliver just-in-time to the customer. Most customers preferred getting their supplies just-in-time so as to reduce the inventory holding cost. Eventually it set more than 14 plants across the country.

Once it gained significant market share and became the pre-eminent player in the cable market in India, it began setting its sights on the world. In 2005, It entered into a JV with Gills Cables, a subsidiary of the global giant Carclo which supplied cables to high end cars like Aston Martin and Lotus, which it eventually acquired (discussed below). Also, the entry of global majors like Volkswagen and BMW in India by setting up manufacturing facilities in the country also helped. Suprajit was able to first get a toehold by supplying smaller volumes to these players’ Indian entities. The foreign OEMs were impressed with Suprajit’s quality, cost, design and delivery capabilities and eventually signed them on to their global supply chain. In some cases, it took 10 long years of consistent supply of small volumes to break through into their global supply chain. And Suprajit was nothing if not consistent - its consistent supply of high-quality product in time over years convinced even Japanese OEMs (Yamaha, Honda) to switch majority of their domestic sourcing from their home supplier (Hilux) with whom they had relationship of decades to Suprajit. In fact, Ajith Rai mentioned that Suprajit never lost a client in its entire history.

Once it gained strong market share in the OEM market, it entered the aftermarket segment with the same aggressive focus. While Suprajit was present in the aftermarket segment through OEMs (it supplied cables to OEMs, which then repacked it under their own brand and sold it), it wanted to develop its own brand. The aftermarket segment requires a strong distribution network which it began focusing on in the latter half of the previous decade. However, a thing to be noted here is that cables are generally quite durable and so cables in cars are rarely replaced and the ones in 2 wheelers have a life of three to four years. Thus, the replacement cycle is not that quick.

Tinkering: A feature we love in businesses is the willingness to tinker. Tinkering as described by Taleb is an activity with low downside and high upside - like having a cheap call option on huge upside. Suprajit, in the beginning of this decade set up a technology center whose aim was to develop new products or segments that it could enter, in addition to developing upgrades on existing products. The products developed were introduced into the aftermarket to piggyback on the distribution network and the brand of the business. While no product has become very successful, the efforts continue. It has recently developed its own parking levers and gear shifter cables for which they are in talks with various OEMs.

Team Suprajit:

An aspect where most exceptional entrepreneurs falter is building a team and delegation. While the founder of the business has an exceptional impact on the business in the early stages of growth, once the business reaches a scale, delegation is key. At some point, tasks have to beassigned to various employees if the company has to transition to the next level.Ajith Rai’s long-term thinking is evident in this as well. His commentary in conference calls and in the annual report repeatedly talk about the ambitions and strategies of ‘Team Suprajit’. Meritocracy is indicated by the fact that senior employees (Dr. C Mohan and NS Mohan) have been appointed on the Board of the company in recognition of their services and long-term thinking. A long-timer in the organization Narayan Shankar was elevated to the post of COO (post created for him) in recognition of his contribution, and similarly, Medappa Gowda, the long-term VP of Finance was made the CFO.

Recently, the Board at Suprajit decided to separate the post of Chairman and Managing Director. With this, Ajith Rai was appointed as the Executive Chairman while NS Mohan, took over the role of Managing Director. This was because of the Board’s belief that the increased scale of Suprajit’s operations required two senior members to manage it.

Another interesting feature observed about Ajith Kumar Rai is the appointment of couple of Board members. In 2002, Suprajit acquired Shah Concabs, a competitor in the cables space which was into heavy duty cables for the 4 wheeler industry. After the acquisition, SN Shah, the erstwhile owner of Shah Concabs was appointed on the Board. Similarly, after Suprajit acquired Gills Cables, its JV Partner in Europe, Ian Williamson (CEO of Carclo, the owner of Gills Cables) came on Board of the company. All this when it had a market cap of less than 100cr ($14 million).

Ajith Rai’s two children have joined the business a few years back. They were not directly given the top posts in the business. The elder son (Akhilesh Rai) started off in IT before finishing his MBA and joining as the Chief Strategy Officer. The younger son (Ashutosh Rai) is currently the Head of New Product Development.

Acquisitions:

Acquisitions have historically been a major part of the growth in Suprajit. It has done 4 major acquisitions till date. Below is a compilation of the rationale as expressed by Ajith Rai in various conference calls.

"Globally, we will only be looking at cable business or something related to cables. We need to get better positioning in global market. Domestically, we are looking at other segments as well. But we are very clear about what we would not do. We do not want to buy any forge shops or something like that where the pricing of the end product can easily be determined by the end customer. We are looking at products that are assembled and where the pricing is not easily determined by the end customer. We want a business which has a margin profile similar to ours or where we see a roadmap of being able to take the margin profile closer to ours. The acquired business should be in top 2 in the segment with good standing in the market and with good potential for growth. We are not experts at turning around businesses or going into debt ridden companies and making things work and all that.

We did have quite a few proposals, some of them we liked, but basically it got stuck where the valuations since came into picture. I think I look at the business and then I compare with myself, and I say that if I am spending x dollar in Suprajit and growing the business by so much with so much margin, if I have to invest same x dollar somewhere else, I should at least match it, right? Unless I get that kind of valuation, I don’t think we will look.So, you know, I am not here to do an acquisition for the sake of acquisition. We are fairly conservative. We have intent to acquire but not desperate. We have looked at number of options over years and rejected - either due to valuation or because of complexities in operations which made us worry about integration."

Shah Concabs: This was acquired in 2002. As opposed to Suprajit which was a major player in the 2 wheeler cables segment, Shah was in the automotive segment. It also gave Suprajit presence in the Western part of the country where they did not have presence. This was acquired for an amount of 5cr ($700k).

Gills Cables and JV: Gills Cables, a UK based cable maker and the JV with Gills (Suprajit Gills) was acquired by Suprajit in 2006 for an amount of 20-25cr (~$3-3.5 million). The JV was formed to set up manufacturing facility in India, which would then supply cables at lower cost to Gills (renamed to Suprajit Europe), that would serve as the consumer facing and warehousing arm. This gave Suprajit access to the European market and was the first major step in the progress towards becoming a global player. The subsidiaries together are performing well with having paid for themselves comfortably. Suprajit has used the acquisitions as a base for its international strategy and today supplies considerable volumes to BMW, Volkswagen, GM, Renault-Nissan and Ford. This is currently the fastest growing part of the group currently and the profits generated by them today are equal to the cost of acquisition.

Phoenix Lamps: From the end of the previous decade, Suprajit was on the lookout for an acquisition candidate outside of the cable space. It realized that its days of growing at a rate of 5%-10% faster than the industry would soon be over if it concentrated just on the cables segment. So it decided to look out for acquisitions as it is extremely difficult and time consuming to dislodge an existing supplier to an auto OEM.After years of search, the team at Suprajit decided to acquire Phoenix Lamps in 2015. Suprajit bought this asset from a private equity (PE) player Actis. Like most PE players, Actis had a limited time horizon and with Phoenix, it had reached that limit after around 8 years. It is interesting to note that Actis sold its entire stake of 62% to Suprajit for 154cr, less than half the price it had paid in 2006-07. Clearly, Suprajit had acquired from a forced seller. At the time of acquisition, Phoenix had debt of 56cr (~$8 million), sales of ~340cr (~$50 million), EBITDA of ~47cr (~$7 million) and profits of 20cr (~$3 million).Phoenix had a lot of characteristics Ajith Rai was looking for; in fact he said, “It was like seeing a mirror image of Suprajit.” Phoenix was into the halogen lamp space primarily used in the headlamps of vehicles. It was an assembled component and had margin profile similar to that of Suprajit. It had a strong market position with capacity of 85 million and a similar customer profile. Also, similar to cables, lamps were a mass manufacturing product. The balance sheet was also good with only working capital debt. Phoenix generated around 66% revenues from export aftermarket - it sold lamps in Europe under the brands Trifa (primarily Germany) and Luxlite (other countries); around 23% from sales to domestic OEMs and 11% in domestic aftermarket. It had a large market share in both OEM and aftermarket space in India.The strategy was to go after the large aftermarket- there are about 800 million vehicles plying the roads globally with each having 4 halogen lamps. The life of each lamp is around 3 to 4 years. And Phoenix has a minuscule portion of the market.However, there were issues as well. The PE player had heavily under-invested in the plant and equipment for 2 to 3 years prior to the acquisition. This resulted in Phoenix losing clients in the year it was quired due to quality issues. Also, there huge huge contingent liabilities of 86cr (~$12 million) in the form of disputed tax demands.Then there was probably a long-term trend of the market moving to LED bulbs. Here is the CEO NS Mohan’s take on the LED risk:

“In the lamps as we were talking about it, we see a substantial headroom for growth in the global aftermarket. Of course we have a core position in the domestic aftermarket, now what we are trying to do is enhance the footprint, not just Europe but also to US. LED is going to come that is the fact of life, now we cannot wish it away, so we do see us losing OEM business slowly over time. But there is going to be a substantial population of vehicles, which still have halogen bulbs that needs to be serviced. People like Phillips would be moving away from it; therefore, the big players as they move there should be somebody who needs to get into that vacuum and take that business and we feel as Phoenix that we need to do it and that is where I see a headroom for growth.”

The wrinkle in the Phoenix saga: In the initial quarters after the Phoenix acquisition, Suprajit management mentioned they were not looking to merge it into Suprajit anytime soon. But within a year of the acquisition, Suprajit board decided to merge Phoenix with itself. This was to reduce the monetary and time cost of managing two separate listed entities. The merger ratio was set at 5 shares of Phoenix for every 4 shares of Suprajit, at an implied price of 110 per share for Phoenix based on the then price of ~130 per share of Suprajit. This was higher than the regulator recommended price of 103-105 and the 89 per share Suprajit paid Actis. Thus the ratio was legally fine.

However at the time of the decision to merge, Suprajit was richly valued at more than 20x P/E and 3x sales, while Phoenix was still not performing at its best. However, it is pertinent to remember that Phoenix had to invest around 30cr (~$4.3 million) in its plant and the huge contingent liability.When the merger was announced there was disgruntlement among some Phoneix shareholders who felt they were shortchanged as they were receiving expensive Suprajit stock in return for the cheap Phoenix stock.

Subsequently, in Feb 2016 (a year after the acquisition) Suprajit further issued shares to a few institutional investors at the rich valuation of Rs 133 per share to raise 150cr (which almost the amount spent to purchase Phoenix Lamps). This was done to strengthen the balance sheet and position itself for further acquisition opportunities that may arise.

Overall, the acquisition of Phoenix indicated the capital allocation intelligence of Team Suprajit. With hindsight we see they used expensive currency, Suprajit stock, to purchase the entire Phoenix Lamps shares - first from a forced seller (62% from Actis) and the remaining from the public.But the business quality is in our opinion was not comparable to Suprajit’s so far given the high exposure of the business to Europe.

How has the business performed?

The first couple of years went into bringing Phoenix operations back on track by correcting the under-investment done by the previous owners. Suprajit went to work modernizing the plant and bringing manufacturing standards up to par. They successfully resolved the tax issues as well. It is a testament to the operational skills of the team that Phoenix is today generating margins comparable to Suprajit’s on a sustainable basis.While the operations, improved the growth has been quite muted due to the large Europe exposure and the loss of customers at the time of acquisition (due to quality issues and unavailability of new designs). It also did not help that certain Indian OEMs like Honda Motorcycle shifted to LED in their mass market vehicles (as opposed to management expectation of niche vehicles) whichreduced the OEM business.

In 2019, the acquisition generated sales of around 320cr and EBITDA of 40cr, as compared to 324cr and 44cr respectively in the previous year. Cumulatively, the company has generated EBITDA which is about 50%-60% of the EV paid for its acquisition. Thus broadly, the payback period seems to be pretty average in retrospect. But probably the slowdown in Europe is going on longer than the initially anticipated. To counter this, Suprajit is attempting to enter the Russian and US aftermarket thus enlarging the addressable market.

Wescon: On the heels of the merger with Phoenix Lamps, Suprajit announced the acquisition of Wescon Controls from a PE player. Wescon, is Kansas based leading designer and manufacturer of mission-critical mechanical cable and electronic controls for the North American outdoor power equipment (OPE) market. It is a very strong brand in its space with a market share of 50%-60% due to its 70-year history. It had 2 plants in Wichita, Kansas and Juarez, Mexico. It had sales of $40 million and EBITDA margins of 16%-18%, and Suprajit acquired the business at an enterprise value of about $44 million. It used acquisition debt at Wescon of about $25 million to consummate the acquisition.

Suprajit’s plan was to use Wescon as the foundation to launch an aggressive non-automotive cable strategy . The existing non-automotive cable business was bunched into Wescon, and was named Suprajit Engineering Non-Automotive or SENA. Under the segment, Suprajit would use the Wescon brand and extend into other non-automotive segment apart from OPE, spaces where Wescon had limited current presence. The strategy was to offer customers three plants (India, US, Mexico) from which they could source products depending on their preference, with the long-term goal to develop a strong market position in this space as well.

Suprajit continues to scour for acquisitions and here is the rationale in the words of Ajith Rai:

"It is not necessarily new product that we are looking for acquisitions. We are very clearly focusing on those that are strategic to our core business. Globally there is a lot of consolidation of supply is happening. The major customers want to have a very strategic supplier who is capable of delivering them from multiple geographies. I think that is the crux of the matter, the big guys want to have three or four who can supply to their – who are financially and technically capable to deliver them to anywhere in the world, I think that is where we are positioning ourselves and we are trying to see that where we have a gap in filling those requirements of the customers.Not that we would not look at new product, but at this moment we are focusing on seeing how we can be more sustainable supplier to our key customers globally on our existing products.

It is not the growth of the business alone that is our focus. It is strategic fit and position of the asset also that matters. For example, we do a lot of business today and we think probably it is not enough to have just a warehouse in Europe. It might be better to have a manufacturing facility closer to the customers which will increase the customer comfort.I can say that in cable, can say is that one-third of the business in North and South America, one-third of the business is in Europe, one-third is in Asia, so we are strong in Asia, we are trying to see what else we can do."

Electric vehicles and Sensors risk:

One worry in the auto component space is the electronification of parts and the electric vehicle risk. Here is Ajith Rai’s comments on that perceived risk:

"We are perennially on the lookout for changes that are happening in our businesses. Cables is our first product and we have reviewed it regularly over the last 35 years. In terms of electric vehicle the only change is in the engine pack, the ICE engines gets changed with an electric pack whatever that is, so as it is on an ICE engine at the engine and at the transmission level, we do not have a cable, so when it gets replaced with the another new technology whether it is electric vehicle or anything else it does not really affect, so we do not really see a threat per se by the change over to electric vehicle

Also, we have observed that over time the number of cables have only increased over time. In both cars and 2 wheelers both we have seen this trend. For example, till recently I used to say each 2 wheeler has 4-5 cables, but with a few recent changes, in the next two years I expect it to become 5-7 cables. Similarly, a car used to have 3-4 cables when we began our business, it increased to more than 10 and in some cases it is increasing to 15 today. It is not that the applications are the same. Because of technological changes, some applications are changing and going away - there are hardly any clutch cables, lesser transmission cables, etcetera, but new applications are replacing these.

You see cables have been found to be the most cost effective, NVH (noise, vibration and harshness) compliant way to move a part from one end to other end or moving some kind of load within the vehicle. While we keep assessing this in the context of customer’s requirements what we see is the applications have increased and we do not think cables will stay for a long period of time".

Now, let us recap how Suprajit went about de-risking its business model over the last three decades:

It began as a cable manufacturing company with a single plant in a single location (Bangalore) supplying to a single customer (TVS) in a single segment (2 wheeler OEMs).

Then, it became a company with plants in multiple locations, supplying to multiple customers in the same segment (2 wheeler OEMs).

Then, it evolved into having multiple plants in multiple locations supplying to OEMs in 2-wheeler, 3 wheeler and 4 wheeler space.

Then, it began selling its cables to international customers as well.

Then, it entered the non-automotive, non-2 wheeler space by winning large orders from John Deere which steadily increased the business to Suprajit due to its quality cost, delivery and design.

Then, to diversify away from just cables, it acquired Phoenix Lamps, a halogen headlamp manufacturing company with operations in India and Europe. The acquisition was in the automotive space itself.

Then, it acquired Wescon, a market leading manufacturer of control cables in the non-automotive outdoor power equipment (OPE) space, supplies to leading global OEMs such as Husqvarna, John Deere, Toro, Honda, etcetera. Wescon also has manufacturing facilities in the US and Mexico.

From a single brand (‘Suprajit’) which supplied cables to OEMs, the company today has three brands - Suprajit for automotive cables, Phoenix (with the sub brands Trifa and Luxlite) for halogen lamps and Wescon for non-automotive cables.

Financials:

It says something about the execution skills and the growth focus of the team at Suprajit that ever since its inception it has grown at a rate of 5%-10% above the Indian automotive industry growth. The sales have grown from 25cr ($3.5 million) in 2001 to 1,600 cr today ($230 million) today. While the profits have grown from 2.2cr ($300k) to 130cr ($19 million) today. During the entire period the EBITDA margins has remained in a tight range around 16%. This is despite the fact that there is no automatic pass-through of price increases to OEMs, each price increase is negotiated. This indicates the tremendous internal cost efficiencies that the group has been able to generate over the past three decades. The growth was never achieved at risk to the business, the net debt-to-equity and EBITDA/Interest indicators have remained quite comfortable at <1x and >5x throughout.

The true quality of the business is evidenced by the fact that the average returns on equity and capital of the business over the last decades has been higher than 25%! This fact explains the tremendous market cap growth in the business as over the long term, the returns on a stock reflects the return generated by the business.

Conclusion:

Suprajit today dominates the niches it operates in - it has more than 40% of the cable market in India with around 70% market share in 2 wheelers and 30% market share in automobile segment. It is more than 3x the size of its next largest competitor domestically. Wescon has more than 50% share in the OPE segment. Its subsidiary Phoenix has 60%-80% share in the OEM segment of the halogen lamp business in India and more than 50% of the organized aftermarket business in India. Phoenix’s production capacity is almost 3x the next largest competitor’s capacity in the country.

And it is keenly searching other niches to dominate globally. In cables business, its global share is still very small (~$25-30 million in comparison to >$2 billion). In the non-automotive cable segment, it intends to enter the power sports vehicle and the medical equipment segment through the Wescon brand. Even in lamps, it has a pretty small global aftermarket market share which is the focus currently, where it intends to position itself as a high quality alternative on par with Korean suppliers at a much more competitive price - Korean quality is considered best while Chinese costs are the lowest. Phoenix is positioning itself as best quality at much lower price.

From 2003 till 2019, the market cap of Suprajit has jumped from 15cr ($2 million) to 2300cr ($300 million) with minimal dilution. And we believe the journey is not close to being over.